Vietnam Seafood

Strong demand from China and the U.S. drives Vietnam’s pangasius export growth

19

May

May

According to data from Vietnam Customs, in March 2025, Vietnam’s pangasius exports reached USD 182 million, up 21% from the previous month and 16% year-on-year. Robust demand from Vietnam’s two key export destinations – the United States and China – continues to play a pivotal role in driving the outbound flow of pangasius products beyond national borders.

The temporary 90-day suspension of the proposed 46% countervailing tariff on Vietnamese goods has provided exporters with a crucial window to ship their products to the U.S. and explore alternative market opportunities.

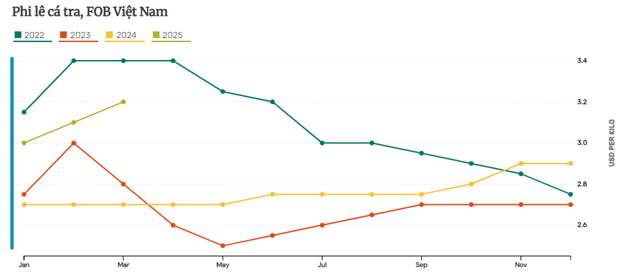

Currently, the export price of pangasius to the U.S. is approximately USD 3.40/kg. If the 46% tariff is implemented, the price could rise to around USD 5.10/kg—rendering Vietnamese pangasius significantly less competitive against other whitefish products. This scenario could result in substantial losses for exporters, where increasing export volume paradoxically exacerbates financial hardship. As a result, enterprises may be compelled to reassess their market strategies, potentially reducing their exposure to the U.S. and shifting focus to other regions.

In terms of volume, Vietnam’s pangasius exports across all markets experienced a sharp increase in March 2025, rising from over 55,000 tonnes to nearly 79,000 tonnes – an impressive 23% year-on-year growth.

Most major export markets recorded notable month-on-month increases in March 2025: China & Hong Kong: +61%, ASEAN: +11%, United States: +28%, European Union: +73%, Brazil: +44%, Mexico: +15%, United Kingdom: +120%. This surge in export volume was partly due to the absence of disruptions caused by Vietnam’s extended Lunar New Year holiday, which had affected shipment volumes in the first two months of the year. Additionally, rising demand from China toward the end of March was supported by a decline in raw material prices.

Looking ahead to April 2025, raw pangasius demand may soften among major U.S.-bound exporters due to ongoing tariff-related uncertainty. Nevertheless, the China & Hong Kong market is showing signs of improved supply conditions, suggesting that overall demand for raw pangasius may remain resilient.

The average export price for all pangasius products rose by 2% in March, reaching USD 2.28/kg.

Thanks to a strong rebound, China & Hong Kong regained their position as Vietnam’s largest pangasius export destination in March 2025, importing over 21,000 tonnes. This followed a notable drop in February, which marked the lowest monthly import volume in the past year.

However, the average export price to China decreased by 4.2% to USD 2.04/kg after six consecutive months of gains. Vietnam’s pangasius exports to China reached USD 38 million in March 2025, up 6% from the same period last year.

By the end of Q1 2025, China and the United States remained Vietnam’s top two pangasius export markets, with frozen fillets continuing to dominate the product mix. Beyond the temporary tariff suspension and trade policy dynamics, consumer demand in both markets remains a decisive factor in shaping retail market trends. Consumers in both countries are familiar with the taste and quality of Vietnamese whitefish. If offered competitive pricing through tariff reductions or trade agreement benefits (e.g., FTAs), their purchasing decisions are likely to shift favorably – thereby boosting both import volume and export value from Vietnam.

Looking forward, there is cautious optimism that Vietnam and the United States will soon reach a mutually agreeable resolution on tariff issues. Concurrently, Vietnam is expected to accelerate negotiations to upgrade the ASEAN–China Free Trade Agreement to version 3.0 (ACFTA 3.0), opening up broader economic and trade opportunities for the region as a whole – and for Vietnam and China in particular.

Source: https://seafood.vasep.com.vn/

Tiếng Việt

Tiếng Việt